Fiscal & Monetary Policy

Government and the Macroeconomy · 4 question types

Exam Frequency Analysis

Past paper frequency (2018 to 2024)

This topic accounts for approximately 16% of your exam marks.

Fiscal and monetary policy are core Section B evaluate topics; expansionary vs contractionary, tools and limitations tested consistently.

Tax is the main source of government revenue, and the way a government taxes shapes every macroeconomic aim. This section covers why governments tax and the main classifications of tax.

Reasons for taxation

Governments do not tax only to raise money. The main reasons are:

- Raising revenue to pay for public services, welfare and infrastructure.

- Discouraging consumption of demerit goods such as tobacco, alcohol and sugary drinks, by adding tax that raises their price.

- Reducing imports by placing tariffs on foreign goods, which protects domestic producers and the current account.

- Redistributing income, by taxing higher earners more heavily and using the revenue to fund benefits and services for those on low incomes.

- Influencing total (aggregate) demand, since raising taxes withdraws spending power from households and firms while cutting them adds it back.

- Encouraging environmental sustainability, by taxing pollution or carbon emissions so that firms have an incentive to pollute less.

Direct vs indirect taxes

A direct tax is paid straight to the tax authority by the person or firm on whom it is levied.

Common examples:

- Income tax (paid on wages and salaries).

- Corporation tax (paid on company profits).

- National insurance (paid on wages, funds social security).

- Capital gains tax (paid on gains from selling assets).

- Inheritance tax (paid on large estates).

An indirect tax is levied on goods and services and paid via the seller, who passes the cost on to the consumer.

Common examples:

- VAT (Value Added Tax): a percentage charged on most goods and services.

- Excise duty: extra tax on specific goods (alcohol, tobacco, fuel).

- Sales tax: similar to VAT in countries that use a single-stage tax.

- Tariffs: tax on imports.

The distinction is who hands the money over to the tax authority. With income tax the worker pays HMRC directly. With VAT the customer pays the shop, and the shop pays HMRC.

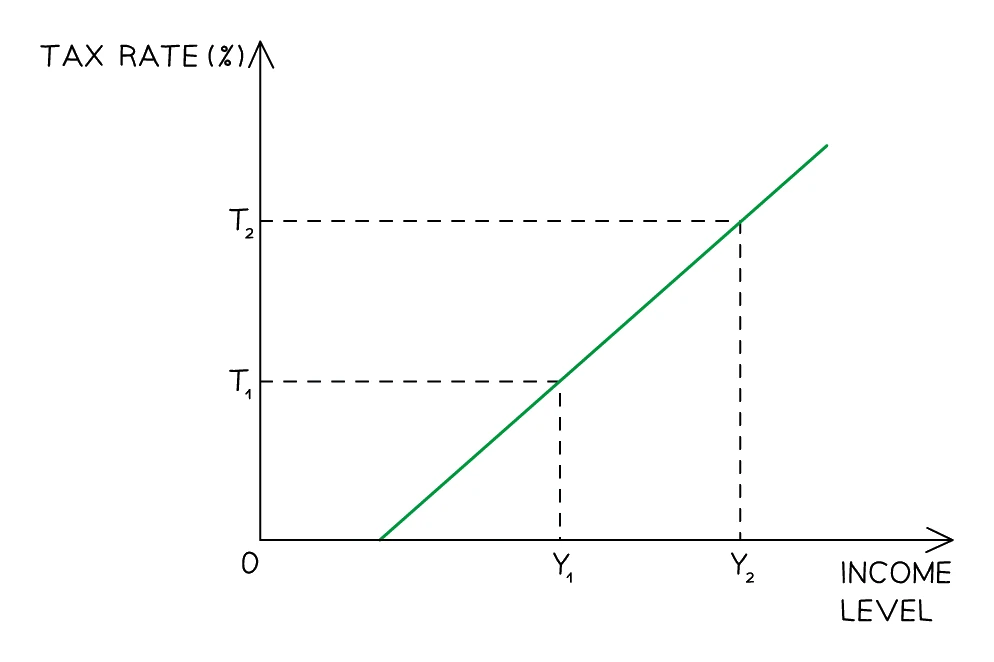

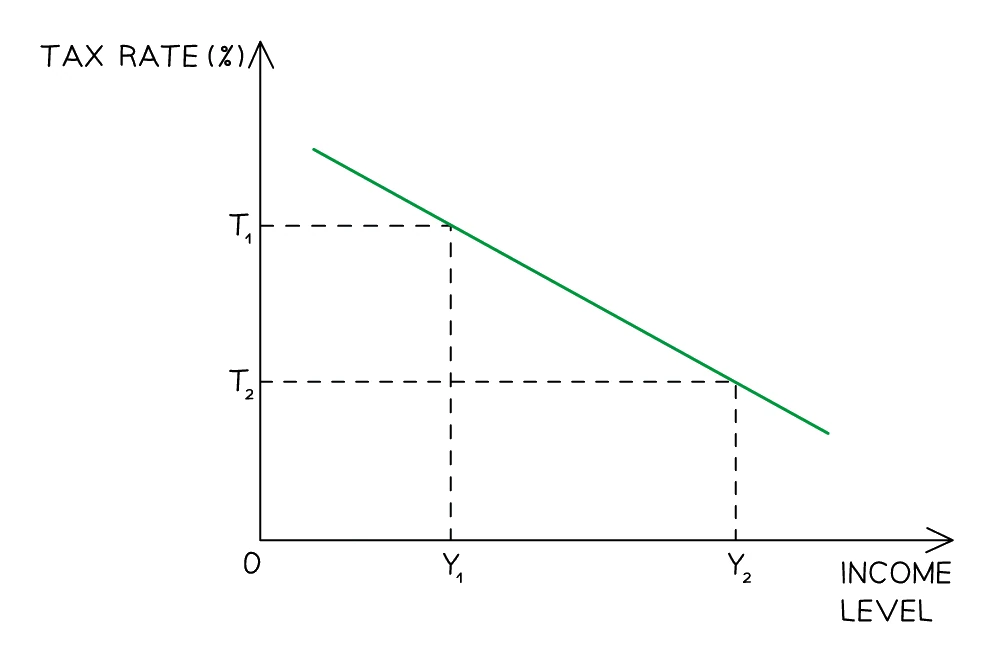

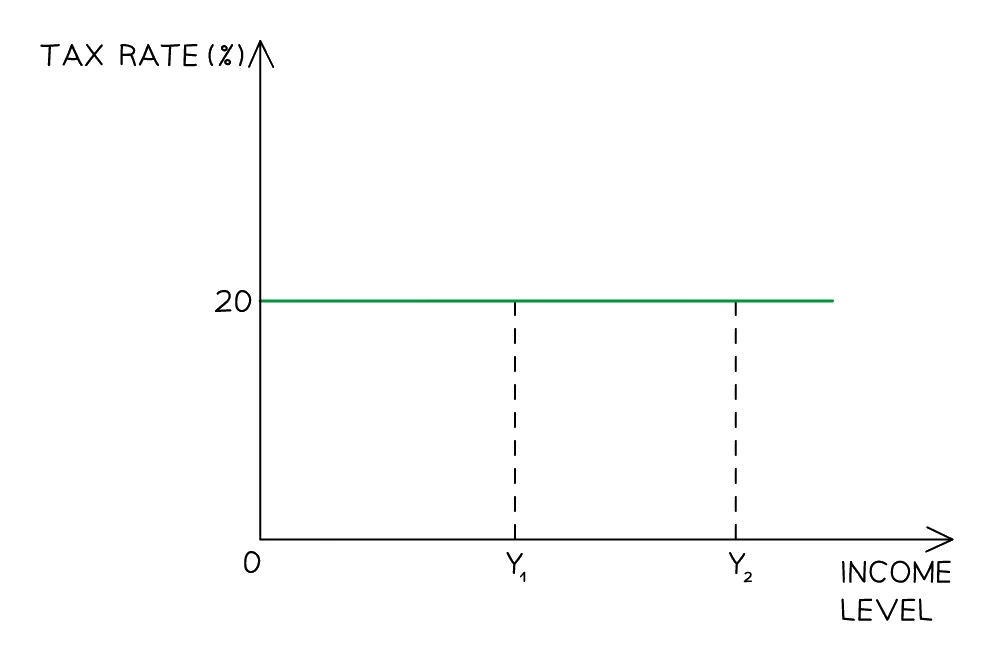

Progressive, regressive, and proportional taxes

This second distinction is about how the tax rate changes with income.

A takes a higher percentage of income from the rich than from the poor. Income tax with rising bands is the classic example.

A takes a higher percentage of income from the poor than from the rich. VAT is regressive in practice because poor households spend a higher share of their income on taxed goods.

A takes the same percentage of income regardless of income level. A "flat tax" on all earnings would be proportional.

Direct vs indirect: strengths and trade-offs

| Direct tax | Indirect tax | |

|---|---|---|

| Usually progressive? | Yes (income tax with bands) | No (often regressive) |

| Visible to the taxpayer? | Very (PAYE on payslip) | Less (built into prices) |

| Distorts consumer choice? | Less | Yes (consumers shift away from taxed goods, useful for demerit goods but problematic otherwise) |

| Can be avoided? | Hard (employer deducts at source) | Easier (the informal economy escapes VAT) |

| Stable revenue? | Yes (predictable from wages) | Yes overall, but falls in a recession when spending falls |

Most countries use a mix of direct and indirect taxes to fund the public sector.

Identifying types of tax (2 marks)

What comes up: a 2-mark question asking you to identify or name two types of tax.

Write: name any two from either classification. From the direct/indirect split: (1) direct tax, (2) indirect tax. From the rate structure: (1) progressive, (2) regressive, (3) proportional. Mixing the two classifications is fine — e.g. "direct and progressive" counts as two correct types.

Watch out: naming only examples (e.g. "income tax" and "VAT") without labelling the type of tax may not score without the classification word. The mark scheme accepts specific tax names as examples that illustrate a type, but the type label itself (direct, indirect, progressive, etc.) is the credited answer. If the question asks you to "identify two types", write the type name first.

Impact of taxation

Tax changes ripple through the whole economy:

- Consumers pay more for taxed goods (indirect tax) or keep less of their income (direct tax), so their purchasing power falls. Higher taxes on demerit goods are meant to cut consumption of those goods.

- Workers may have less incentive to work or work overtime if income tax rises sharply, though most still work because they need the income.

- Producers and firms face lower after-tax profits from corporation tax, which can reduce investment; indirect taxes raise their selling prices and may cut sales.

- The government gains revenue to fund spending, but very high tax rates can encourage avoidance and evasion, which reduces the revenue actually collected.

- The economy as a whole sees aggregate demand fall when taxes rise and rise when taxes are cut, which is exactly how fiscal policy works.